Your neighbor’s solar panels shouldn’t be costing you money, they should be lowering the cost of power. If solar and other distributed energy resources (DERs) are properly incentivized to work for the grid, they should decrease the amount of dollars that utilities need to invest in infrastructure, which impacts rates. But with Net Energy Metering (NEM), non-solar customers are being burdened with higher shares of the rate base instead of benefitting from the investment. Are these costs they should be paying in the first place? This debate is currently playing out in California, kicked off with the En Banc Report.

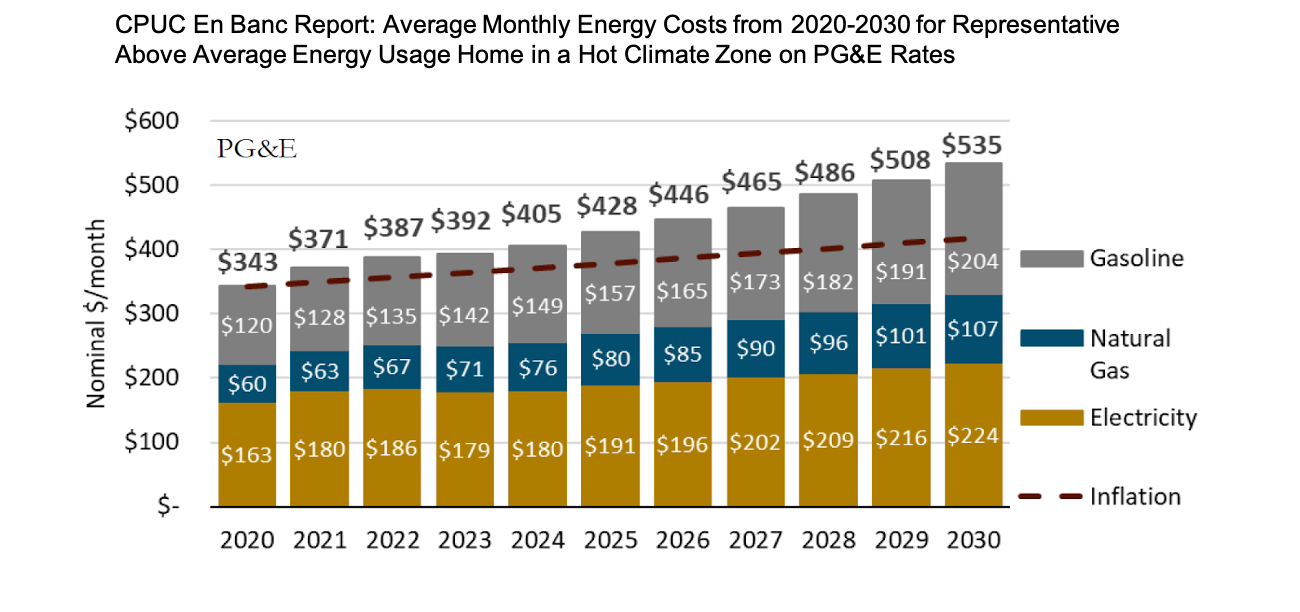

DERs aside, utility rates and bills have been increasing in the state. While bills in California were considered low nationally, mostly due to the success of energy efficiency programs, that expectation is quickly changing. The increase in energy costs that are outpacing inflation are expected to continue for the foreseeable future and thus are expected to increase customers' bills and reduce affordability. PG&E, SCE, and SDG&E rates’ are expected to increase 3.7%, 3.5%, and 4.7% annually respectively (nominal $/kWh).

According to the En Banc report, this is being driven predominantly by an increase in the rate base. The rate base has been increasing on average by approximately 5 percent per year for PG&E, 8 percent per year for SCE and 7 percent per year for SDG&E since 2016 despite relatively flat load growth.

Essentially, utilities are consistently investing in new assets that are cumulatively worth more than their existing depreciating assets. Which isn’t a problem until you consider Return on Rate Base Revenue Requirement, which maintains that utilities earn a guaranteed return on their rate base in order to reduce risk for investors. However, a set return also incentivizes utilities to maximize their rate base.

The incentives are working, but to achieve what policy goals? A conservative assumption from the report indicates that every $1 put into transmission rate base costs ratepayers in excess of $3.50 over the life of a transmission asset. For example, the $2.75 billion in capital additions for the three California IOUs in 2020 alone can be expected to cost ratepayers at least $9.7 billion over the lives of the assets over a life estimate of 36 years.

While the report doesn’t qualify the validity of these rate-base-increasing investments, it does underscore the rapid growth of both distribution and transmission rate base across all three IOUs and its impact on increasing customer rates.

Thus, the NEM section of the report has been the focus of attention, it is not the driving source of the cost increases. Contrary to the focus of conversation in the regulatory arena, the solution is not the disincentivization of DERs, but the proper incentivization. What is being missed is the opportunity to share infrastructure costs with wealthy residential or large commercial customers that are better able to afford it and then create incentives that allow all ratepayers to benefit from these investments.

Projects like Greenbanks (a public/quasi-public financing institution that utilizes innovative financing and partnership with the private sector to drive clean energy deployment) have shown that each public dollar invested has driven $2.6 of private funding. According to SGIP data from the CPUC (for only their storage incentive in 2020) $1 of public money drove $1.3 in private sector funds conservatively. There is plenty of private sector capital waiting to be deployed for clean energy projects.

However, sharing these costs with private sector wealth will only be effective if these resources are optimized to also serve the grid. Such as focusing resources on developing proper demand response and resource adequacy incentives in California. Microgrids and DERs proved significantly valuable in reducing strain on the grid during California’s August heatwave in 2020. A service that many of these resources were not compensated for. If proper incentives and pathways to participation were in place, even more DERs could have provided service. It is commonly thought that microgrid/DER resilience is a local benefit only for connected customers, but the capacity these resources alleviate during grid strain is a clear counterpoint to that. Existing and future DERs should be properly incentivized to provide resilience benefits to all ratepayers, which can defer other types of infrastructure investments currently being pursued.

Private sector investment in DERs also has the potential to maximize utility-scale investments. According to a report from Vibrant Clean Energy, distributed solar and other DERs will decrease the cost of electricity and the clean energy transition due to increased utilization of transmission investments and deferred infrastructure costs. This is because, with the assumed proper incentives, the distribution grid will seek to maximize benefits by minimizing system operational/infrastructure costs and shifting load. As stated by the report, “the sum of [increased DERs and distribution planning/operation] is net system cost savings, increased jobs, more manageable installation rates, a more reliable and robust system, and more opportunities for private capital investments.” Creating the proper incentives and pathways for participation is going to be the large regulatory hurdle in creating this smart distributed future.

California ratepayers are paying higher rates and bills for a relatively stagnant load and decreasing service (as shown by the 20+ PSPS events initiated in 2020 alone). Building the clean, resilient, and cost-manageable grid of the future will require divergence from how we have typically thought of grid infrastructure investment and grid operation. Instead of focusing on a single incentive, thinking carefully on how to maximize ratepayer value through properly incentivized private sector investment and DER behavior is going to be the great regulatory challenge we must overcome to create the smarter and more equitable grid of the near-future.